PayPal Just Got Wrecked: A Deep Dive Into the 17% Crash

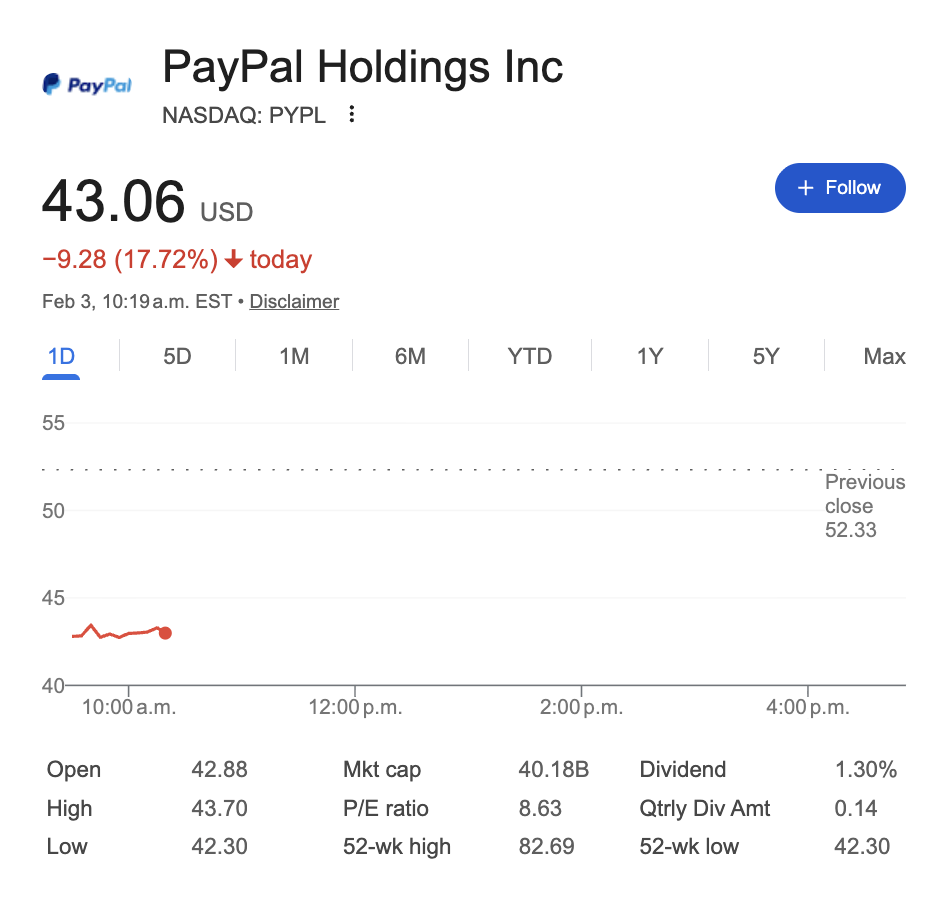

If you woke up this morning and checked your portfolio, I'm sorry. PayPal (PYPL) cratered at the open, dumping nearly 18% and erasing roughly $10 billion in market cap in a matter of hours. The stock went from $52.33 to under $43 before most of Wall Street had their second espresso.

What happened? Well, pretty much everything that could go wrong did go wrong. All at once. On the same earnings call. Let's break it down.

The Numbers Don't Lie (But They Do Hurt)

PayPal reported Q4 2025 earnings of $1.23 adjusted EPS on $8.68 billion in revenue. Wall Street was expecting $1.28 and $8.80 billion, respectively. Not a catastrophic miss in isolation, but when you're a company fighting for its life against a dozen hungry competitors, "close enough" doesn't cut it.

The full-year picture actually looked decent on paper. GAAP EPS rose 35% to $5.41 for 2025. Net income was up 28% year-over-year to $1.43 billion in Q4. But here's the thing about Wall Street: nobody cares about where you've been. They care about where you're going.

And where PayPal said it's going made people hit the sell button.

The Guidance That Broke the Camel's Back

This is where things got ugly. PayPal told investors to expect 2026 adjusted profit to decline in the low-single digits to increase slightly. Read that again. Their best case scenario is "increase slightly." Their guidance range literally includes the word "decline."

For Q1 2026 specifically, they projected non-GAAP EPS to decline in the mid-single digits versus $1.33 in Q1 2025. Consensus was sitting at $1.38. So not only is the full year outlook grim, but the immediate future isn't looking hot either.

When a company guides this far below consensus, it tells you one of two things: either the business is deteriorating faster than anyone thought, or management is sandbagging hard to set a low bar. Given that the board just fired the CEO, I'm leaning toward door number one.

Alex Chriss: 2 Years, Nothing to Show

Let's talk about the elephant in the room. The board didn't just report bad numbers. They fired the guy responsible for them. Alex Chriss, who took over as CEO in September 2023, was shown the door after the board concluded that "the pace of change and execution was not in line with expectations."

That's corporate speak for "you had one job."

The numbers back up the frustration. During Chriss's tenure, PayPal shares dropped 11%. In the same period, the S&P 500 gained 63%. That's not underperformance. That's getting lapped.

To be fair to Chriss, he inherited a mess. PayPal was already in decline when he walked in. Post-pandemic transaction volumes were falling, competition was intensifying from every direction, and the stock had already cratered from its 2021 highs above $300. He was supposed to be the turnaround guy. He monetized Venmo, grew the BNPL business, and talked a big game about innovation. But none of it moved the needle enough.

Enter Enrique Lores: The HP Guy?

The replacement is Enrique Lores, who's been running HP Inc. for the past six years. If that feels like an odd choice for a fintech company, you're not alone. But there's more to it than the headline suggests.

Lores has actually been sitting on PayPal's board for nearly five years and served as Board Chair since July 2024. So he knows the business. At HP, he navigated a hostile $35 billion takeover bid from Xerox, led the company through COVID, and pushed into AI computing. The guy knows how to restructure and cut costs.

His stated priority? "Improve our performance and grow our share in branded checkout, which is the core business of the company." At least he's correctly identified the problem. Whether he can fix it is another matter. He officially starts March 1, with CFO Jamie Miller holding down the fort until then.

But here's my concern: PayPal doesn't need an operational efficiency expert right now. They need someone who can out-innovate Stripe, Apple, and a dozen other companies eating their lunch. Lores is a steady hand, not a visionary. Time will tell if that's what PayPal actually needs.

The Real Problem: Branded Checkout Is Dying

Forget the CEO drama for a second. The existential threat to PayPal is right here: branded checkout growth slowed to roughly 1% in Q4, down from 6% a year ago.

Branded checkout is PayPal's crown jewel. It's the PayPal button you see on every e-commerce checkout page. It's high-margin, high-volume, and it's what makes PayPal... PayPal. When that button stops growing, the entire investment thesis wobbles.

So why is it slowing? Three reasons:

1. Apple Pay is eating the mobile checkout alive. Apple holds 55% of U.S. mobile wallet users. PayPal and Venmo combined sit around 30%. When you have an iPhone (which is most of America), paying with Apple Pay is frictionless. Just a double-click and Face ID. PayPal can't compete with that level of integration. Apple owns the hardware, the OS, and the wallet. Good luck competing with that.

2. Stripe is winning the merchant side. Stripe is now valued at $110 billion. PayPal's market cap? $50 billion. The company that powers the backend for most of the internet's fastest-growing businesses is worth more than double the company that pioneered online payments. Stripe's developer experience is leagues ahead, and younger companies are building on Stripe from day one.

3. Consumer spending is softening. High interest rates, sticky inflation, and a wobbly job market mean people are spending less on discretionary purchases. When total e-commerce volume growth slows, PayPal feels it disproportionately because they're already losing share within a shrinking pie.

The "Agentic Commerce" Hail Mary

PayPal's big strategic bet for 2026 is something they're calling "Agentic Commerce." The idea is that AI shopping agents will handle purchases on your behalf, and PayPal wants to be the trust layer, the payment method these AI agents use when they buy stuff for you.

They even acquired a company called Cymbio in early 2026 to build out these capabilities. It's a real strategy, and in theory it could work. AI-driven commerce is coming whether we like it or not, and there's a genuine need for a trusted payment intermediary in that world.

But here's the problem: analysts don't expect any of this to materially impact the business until fiscal 2027 at the earliest. That's a long time to wait when your core business is decelerating and your stock just lost a fifth of its value overnight. You can't pay your shareholders in roadmaps.

Down 81% From All-Time Highs

Let's zoom out for some perspective. PayPal hit its all-time high above $300 per share in mid-2021. Today it's trading around $43. That's an 81% decline from peak to trough.

The pandemic was both the best and worst thing that happened to PayPal. It pulled forward years of e-commerce adoption, inflated the stock to unsustainable levels, and then left the company exposed when the world normalized. The 2021 highs were a sugar rush, not sustainable growth.

Now the company is stuck in this purgatory where the stock is "cheap" on traditional valuation metrics but there's no catalyst to make it go up. Revenue growth is 4%. Branded checkout is stalling. The new CEO hasn't started yet. And the competitive landscape gets worse every quarter.

What Happens Next?

Among 45 analysts covering PayPal, only 13 rate it a buy. 27 have it at hold. 5 say sell. That's about as lukewarm as analyst sentiment gets. Nobody wants to pound the table on this name right now.

The bull case is straightforward: at $43, you're getting a company that still processes $475 billion in payment volume per quarter, generates real profits, and has a brand that hundreds of millions of people recognize. If Lores can stabilize branded checkout and the AI commerce bet pays off, this stock could rerate significantly.

The bear case is equally straightforward: PayPal is a legacy payment company in a world that's moving on. Apple Pay owns mobile. Stripe owns developer mindshare. BNPL is commoditized. And no amount of "agentic commerce" buzzwords will change the fact that the core business is in slow decline.

My take? This is a "show me" stock now. PayPal has the scale, the cash flow, and the brand recognition to mount a comeback. But until Lores actually demonstrates he can reverse the branded checkout slide and deliver real numbers, not just guidance and press releases, I'd stay on the sidelines.

The market doesn't give participation trophies. Today's 17% drop made that crystal clear.